Most executives are still looking at China’s AI push through the wrong end of the telescope.

They see model progress, chip constraints, and the usual scoreboard logic. But China’s more consequential move is not simply to build better models. It is trying to build an entire AI economy: the compute backbone, the domestic supply chain, and the everyday use cases that keep the whole machine busy.

That matters because infrastructure without demand is stranded capital, and consumer enthusiasm without infrastructure is a demo. China appears to be pursuing both at once: a reported roughly 2 trillion yuan plan for nationwide data-center expansion over five years, alongside 17 policy measures to push AI into households, retail, services, and consumer devices. The strategic idea is simple and unusually disciplined: do not just fund AI capacity; industrialize AI adoption.

The Quiet Shift Behind the Headlines

The standard story says the AI race is about frontier models. Bigger training runs. Better benchmarks. Faster chips.

That’s only part of the story.

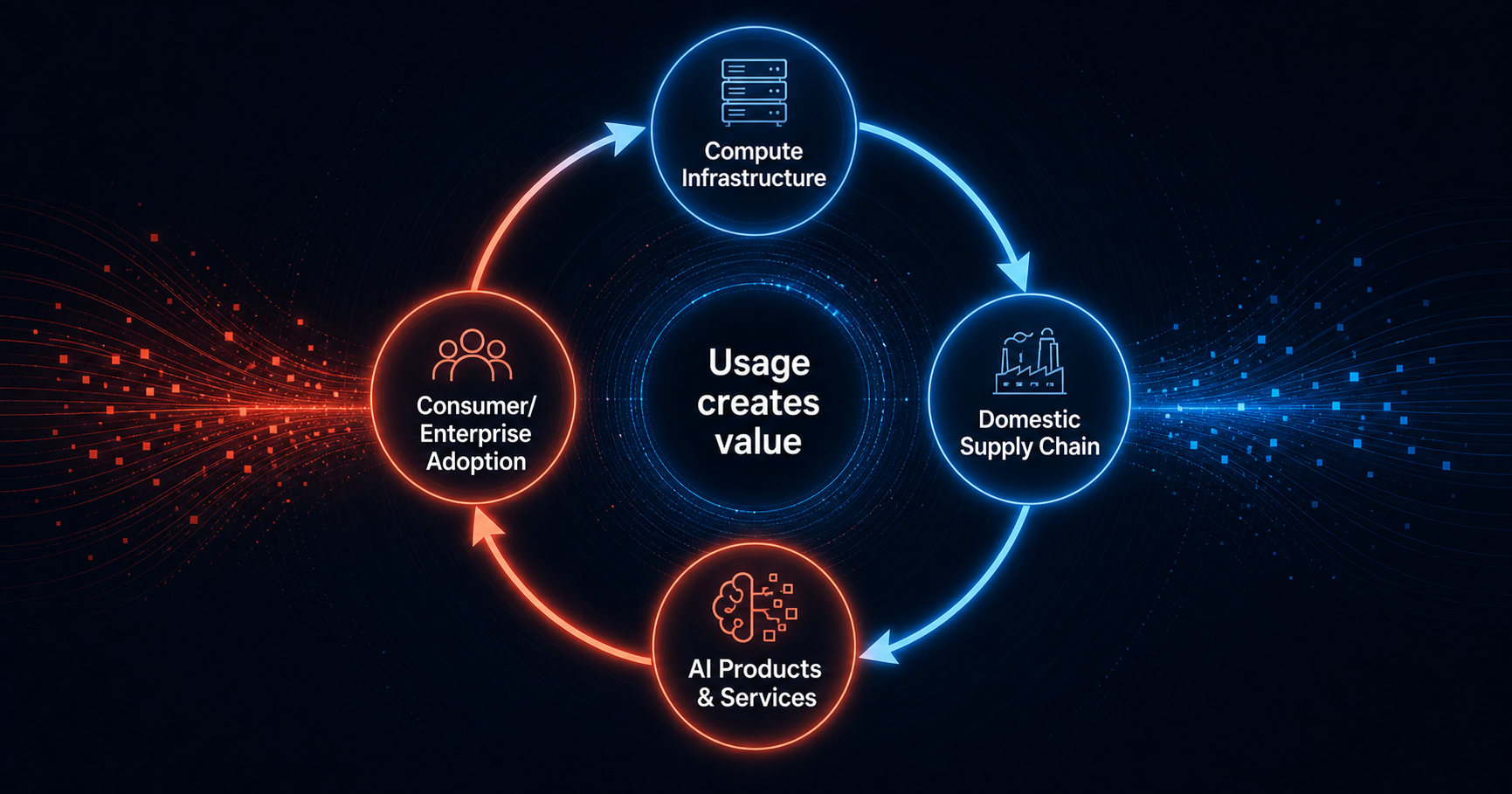

The real issue is who can turn AI into durable, economy-wide usage. A model is potential energy. The hard part is converting it into work. China’s latest moves suggest Beijing understands that better than many market-driven AI strategies do: value does not come from having compute in the abstract; value comes from routing that compute into products, services, and habits at national scale.

This is what makes the story strategically important for C-suites. AI competition is starting to look less like a software contest and more like a contest in system design.

The Real Bet Is Not on Models

China is not just trying to catch up in AI development. It is trying to make AI function as strategic infrastructure and as a demand-stimulus mechanism at the same time.

That is the non-obvious point. Most countries treat AI policy as some mix of research funding, startup support, and regulatory positioning. China appears to be treating it more like rail, power, or broadband: something to be financed, coordinated, localized, and then pushed into broad economic use.

A better analogy is not the smartphone race. It is the buildout of an electric grid. Generating power was never enough; the real breakthrough came from connecting generation, transmission, appliances, and daily behavior into one system. China’s AI strategy looks increasingly like an attempt to do the same thing for compute.

The Race Most Commentators Miss

A lot of commentary still frames this as China versus the United States in a straight model race. That frame is too narrow, and it misses the more durable play.

China’s reported infrastructure push involves interconnected computing centers, state-backed operators such as China Mobile and China Telecom, and a strong preference for local suppliers, with Bloomberg and Reuters reporting Huawei positioned to provide much of the underlying technology. Meanwhile, the consumer-side measures are not about letting adoption happen organically. They explicitly target goods and services, aiming to turn electronics “from functional to intelligent” and expand AI into retail, public services, lifestyle services, and even humanoid robots.

But here’s the thing: this is not simply tech spending. It is coordination. Supply and demand are being shaped together.

How China Is Building the Loop

The mechanism is more practical than ideological.

First, build compute capacity and connect it across regions so it behaves less like isolated server farms and more like a national utility layer. Second, anchor that buildout in domestic suppliers and operators, which localizes the stack and reduces exposure to foreign technology restrictions. Third, create policy-backed reasons for businesses and households to actually use the stuff, so the infrastructure does not sit idle.

That combination matters because AI has a utilization problem disguised as a technology problem. Plenty of countries can announce AI ambition. Fewer can create the conditions for sustained inference demand across millions of daily interactions. China’s consumption measures suggest Beijing wants AI not just in labs or enterprise pilots, but in stores, apartments, devices, and service workflows.

That is why the deeper question is not whether China will “adopt AI.” It is how efficiently it can convert state capital into real usage and then into productivity.

From Compute Capacity to Daily Habit

The evidence is not hidden. Reuters reported that China is preparing a five-year plan worth around 2 trillion yuan, or roughly $295 billion, to build data centers nationwide, while noting the plan is still under discussion and details may change. Reuters also reported that China’s commerce ministry and other departments introduced 17 measures to speed AI integration into consumption, covering both products and services. Bloomberg’s reporting adds the industrial-policy dimension: state-owned firms would operate much of the infrastructure, and domestic suppliers would be central to the buildout.

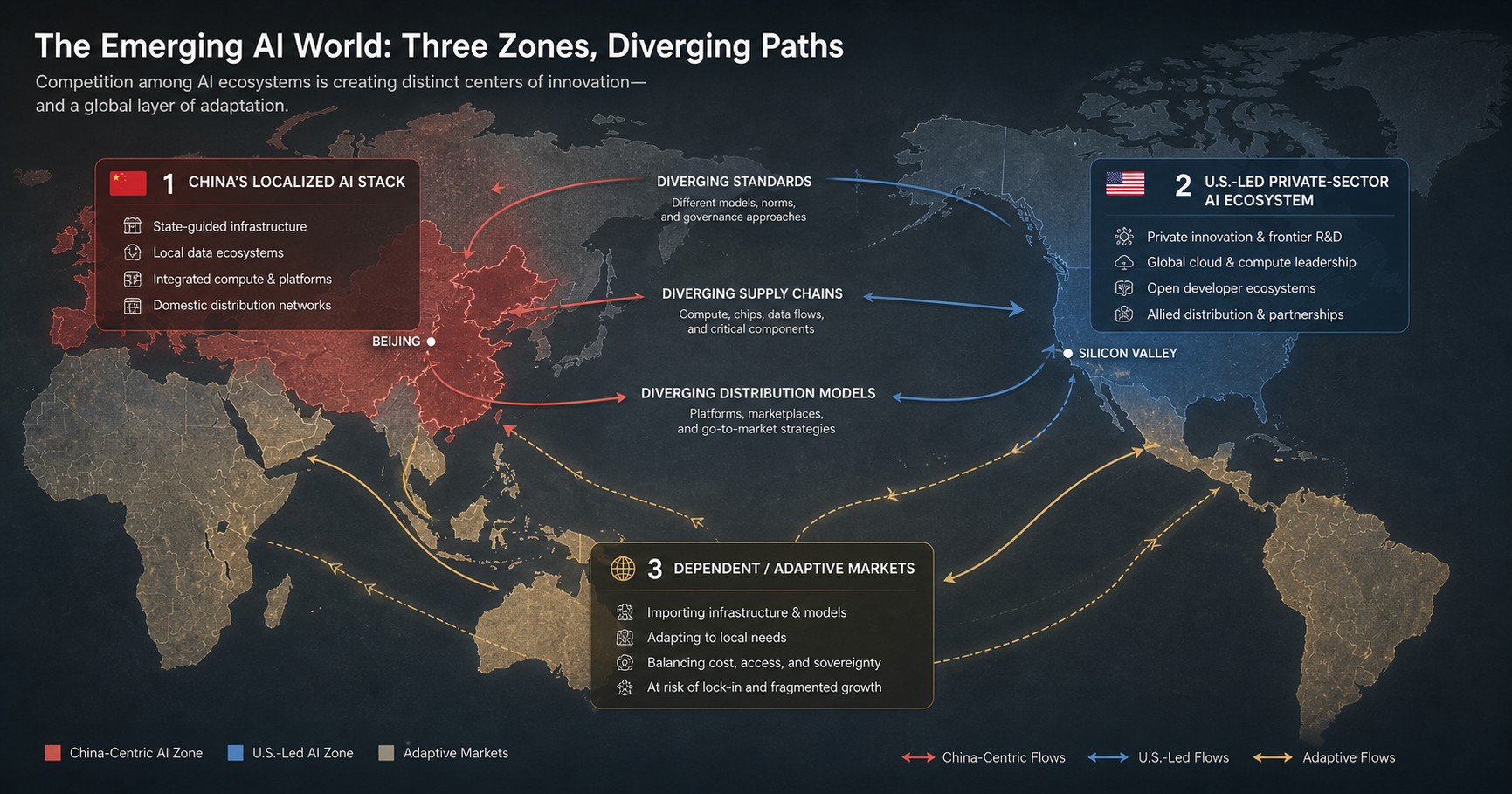

Taken together, those signals point to a more regionalized AI future. Global companies should expect AI competition to fragment into distinct operating environments with different procurement logic, infrastructure assumptions, supplier ecosystems, and policy incentives. The market is not organizing around one universal AI stack. It is starting to split into regional systems.

That has a practical consequence for enterprise leaders. The old question was, “Which model should we use?” The better question now is, “Which ecosystem are we building into, and what dependencies come with it?”

A Separate AI Stack Is Emerging

None of this means China is guaranteed to translate scale into productivity. Big infrastructure plans can create waste, overcapacity, or politically convenient adoption theater. Reuters’ report itself notes the nationwide buildout plan remains in preliminary discussion, and the number should be treated as a reported plan, not a finalized outcome. That caution matters.

Still, the structural logic is real. China is combining infrastructure investment with demand creation, and that is smarter than treating AI as a pure R&D race.

For executives, the strategic takeaway is blunt: AI advantage will belong less to whoever builds the cleverest model and more to whoever builds the thickest loop between compute, distribution, and everyday use. China appears to understand that. Many companies still do not.